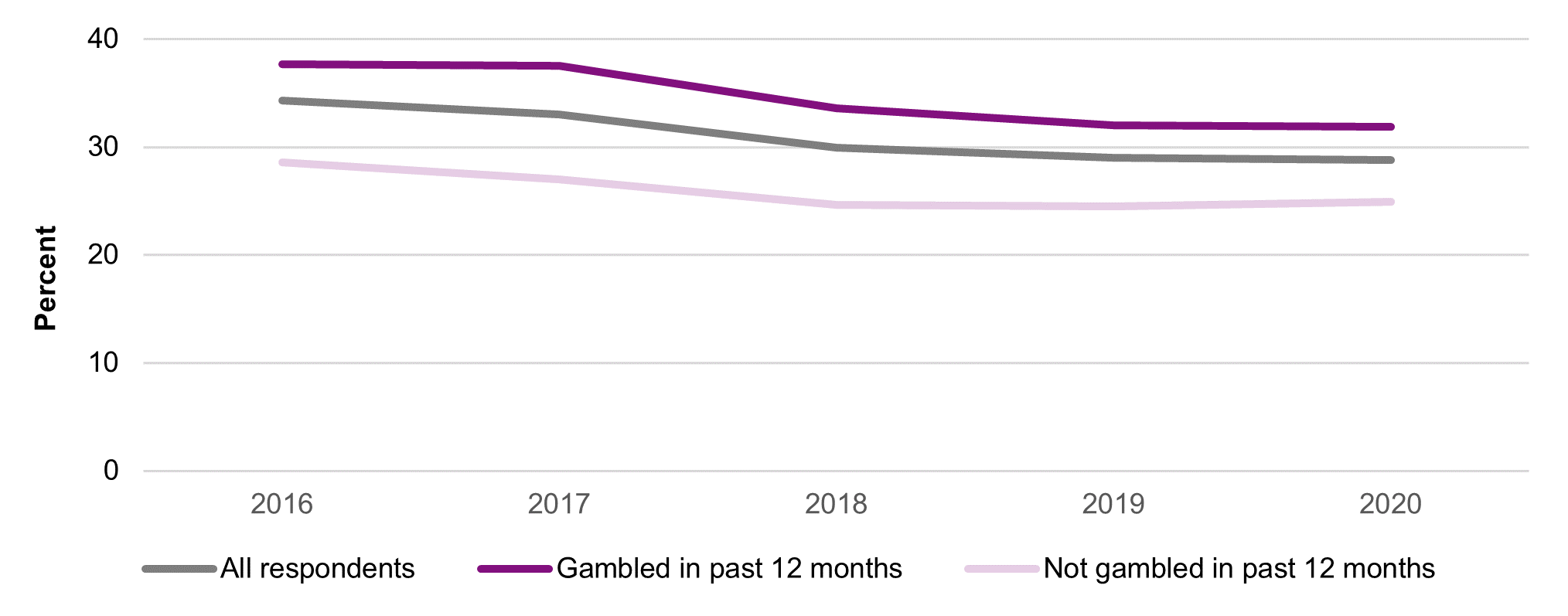

Figure 7 – Respondents agreeing that gambling in this country is conducted fairly and can be trusted

| % | 2016 | 2017 | 2018 | 2019 | 2020 | Significant 2019 to 2020 |

|---|---|---|---|---|---|---|

| All respondents | 34.3 | 33.0 | 29.9 | 29.0 | 28.8 | |

| Gambled in past 12 months | 37.7 | 37.5 | 33.6 | 32.0 | 31.9 | |

| Not gambled in past 12 months | 28.6 | 27.0 | 24.6 | 24.5 | 24.9 |

Although there has not been a significant change in trust in gambling among all respondents between 2019 to 2020, there has been a significant decline in agreement over the past five years, with the agreement rate falling from 34% in 2016 to 29% in 2020.

Socially Responsible Operator(UK/Europe)

Les Ambassadeurs

7. Bet365

- Revenue: £2.81 billion

- Stock ticker: n/a

- Headquarters: North Staffordshire, United Kingdom

- Number of employees: 4646

- Founded: 2000

Bet365 is one of the most successful privately-held betting firms and its boss, Denise Coates, is probably the best paid female executive in the United Kingdom and very much the rest of the world.

Fiscal 2019-2020 ended with £2.81 billion in revenue, a fairly modest dip of just 8.2% amid a raging pandemic. Coates received a hefty remuneration worth £421 million or roughly £48,000 for every working hour.

Coates’ remuneration has made headlines many times throughout the years, subject to divisive opinions. Ultimately, bet365 is a successful sports betting business that treats its employees well and contributes gigantic amounts to Her Majesty’s Revenue and Customs.

9. Entain

- Revenue: €3.57 billion

- Stock ticker: ENT (LSE)

- Headquarters: Douglas, Isle of Man

- Number of employees: 24,000

- Founded: 2004 (as GVC Holdings)

Entain rebranded from GVC Holdings in 2020, opening a new chapter of its story and one focused entirely on sustainability and regulated markets. The company is one of the most substantial FSTE100 gaming firms out there, launching into a number of new markets and seeking to uphold sustainability from the start.

The Entain rebranding came as a result of GVC Holdings’ issues and speculation around a probe looking into potential links with Wirecard. Entain has done well ever since. The company is putting sustainability and player well-being first, and even though it had to see CEO Shay Segev leave early after the rebranding, the company has been able to bounce back by appointing Jette Nygaard-Andersen.

The company’s performance in 2020 remained strong, bolstered by online gaming and Entain’s numerous ventures in the United States, including its participation in BetMGM, now a leading sports betting platform in the country.

Case studies

The Code provides a series of case studies emphasising particularly relevant areas of the GDPR in each. It covers VIPs, problem gambling, direct marketing and fraud detection. While the case studies are not comprehensive, they are useful reminders of some of the key issues to consider.

Sports Betting by Market Share

Soccer betting makes up about 48.4% of the UK’s overall gambling market. Steeplechase and horse racing account for approximately 28% of all sports betting. Tennis betting holds a 5% market share, while dog racing accounts for 3.1%, followed by golf at 0.7%.

A combination of all other forms of sports betting accounts for an extra 9.7% of the UK gambling market. Interestingly, virtual sports, fantasy sports, new sports, and related events have been gaining more popularity. eSports is a particularly intriguing form of sport that has been growing at a rapid rate.

5. Augmented reality

Augmented reality (AR) is one of the hottest topics in both the gaming and gambling industries.

AR technology allows players to experience casino games in a whole new way by placing them in realistic virtual environments.

For example, imagine being able to walk into a virtual casino where you can see other players placed around real-life tables.

This technology is still in its early stages, but it shows great promise for the future of online gambling.

17. Despite American online gambling popularity statistics, 16 states are still unlikely to legalize online gambling.

(Online Casinos Elite)

While it’s true that online gambling is prevalent everywhere in the world, it doesn’t necessarily mean that all of it is legal.

In fact, in America alone, 16 out of 50 states are not even planning on passing a bill, the illegal gambling statistics show. Some of these states are Washington, Texas, Wyoming, Utah, etc.

The UK Gambling Commission’s new rules for September 2022

Changes are coming to the UK gambling market, with the Gambling Commission outlining new rules going into effect on 12 September 2022.

These rules aim to protect at-risk customers and require operators to:

- Monitor a specific range of risk indicators, as a minimum, that identifies gambling harm

- Flag risk indicators and place a requirement to take action in a timely manner

- Implement automated processes for strong indicators of harm

- Prevent marketing and the take-up of new bonuses for at-risk customers

- Evaluate interactions and ensure the operator interacts with consumers at least at the level of problem gambling for the relevant activity

- Provide evidence of customer interaction for high risk to the Gambling Commission

- Comply with these requirements at all times, this includes ensuring the compliance of third-party providers

These changes only affect at-risk customers, so it is unlikely they will have a significant impact on the UK’s Online Gambling market. Operators will have to limit marketing and bonuses for at-risk customers, but the majority of changes will be on a technical side that won’t impact most players. All the details can be found on the official Gambling Commission update.

US Will Become the Key Driver of Sports Betting Growth

Fortunately, legal online gambling is spreading in the US.

H2 forecasts US sports betting operators will reach $1.4bn-$1.5bn in GGR by the end of 2020. It expects that number to nearly double in 2021 and approach $10 billion by the end of the decade.

“Going forward, we can see that resilience playing out and we are now looking at the US as the world’s fastest growing sports betting market,” Henwood added.

Storage limitation

AML and other laws again require operators to keep customer data for specified periods of time which could be longer than customers might expect. The Code says data retention compliance requires an industry-specific approach, especially when determining the start of a retention period. Where accounts are closed at the customer's request or by the operator, the retention period will start at the point of closure.

Industry practice is to keep customer accounts open for indefinite periods, even where the account is inactive. This means that in order to comply with the storage limitation principle under the GDPR which says that personal data should not be retained for longer than necessary in relation to the purpose for which it is processed, operators need to clearly define when retention periods start. AML and other requirements may then define for how long the data is retained and this will vary across EU Member States.

Sector-specific issues with giving effect to the right to erasure are related to those around data minimisation and storage limitation – in some cases, other laws may require that the data is retained for AML, RG and fraud checks.

A particular concern for the EGBA is where a player has multiple accounts across a number of brands. While retention periods for one account may have expired, the data in that account may be relevant to analysis for AML purposes across other accounts. The Code suggests that where the brands are owned by the same company, the data should be retained and that retention periods in the case of multiple accounts begin when the last account is closed or becomes inactive. This would, however, require more detailed analysis as to what the data was originally processed for, who the controller is, as well as its ongoing use during retention periods.

The degree of channelization on the Swedish online gambling market

It is widely acknowledged that a portion of online gambling by people is conducted on sites that do not have a Swedish license, implying that they generally do not comply with the conditions which are stipulated by the Swedish gambling regulation, such as consumer protection routines.

Copenhagen Economics was asked by The Swedish Trade Association for Online Gambling, or BOS (Branschföreningen för Onlinespel), to empirically estimate the degree of channelization, defined as the share of total gambling online that place on sites belonging to entities that are part of the Swedish license system.

The assignment was to use alternative methods to infer the true degree of channelization in Sweden for different gambling categories (verticals) and to assess its development in the near future. The empirical evidence that underpins the findings was collected by a consumer survey, interviews with operators and suppliers on the online gambling market, statistical analysis of gambling volumes provided by market participants, and public statistics from Statistics Sweden, Spelpaus.se, The Swedish Gambling Authority and public enquiries.

Key findings:

Licensed providers are exposed to fierce competition from unlicensed alternatives offering online casino and sports bettingConsumers consider licensed and unlicensed casino sites to be substitutable with respect to trustworthiness and overall product characteristics. Unlicensed casino providers often outperform licensed ones in terms of attractiveness of bonus schemes, which is the most critical factor in marketing, acquirement and retainment of the most valuable consumers.

The odds and other trading conditions in sports betting are very transparent and easily comparable on comparison sites, but there exists some product differentiation between licensed and unlicensed providers.

The unlicensed alternatives in the verticals for horse betting, lotteries and bingo are poor substitutes for licensed sites and have minor market shares.

The overall channelization rate reflecting the situation in January 2020 for all verticals is estimated to be 81-85 percentThe estimated channelization level is broadly consistent with the 85-87 percent estimate by the SGA in November 2019 because their definition of channelization is broader and includes offline sports betting and offline horse betting, where channelization is 100 percent as there exists no real alternatives to ATG and Svenska Spel.

The channelization for online casino is 72-78 percent and decreasingThe development of online casino turnover by licensed operators decreases whereas total online gambling market increases, implying a lower and decreasing channelization level. The estimate is in line with evidence from interviews with operators.

The incentives for operating and starting unlicensed casinos are strong given the restrictions on licensed operators and because of easy of entry to the market.

The channelization for sports betting is 80-85 percent and decreasingLicensed providers have lost 16.8 percent of revenue during 2019 compared to 2018 whereas the total market exhibits steady growth. The degree of substitutability between licensed and unlicensed sites regarding product offerings and winning probability is medium-high despite some degree of product differentiation between providers.

The study is commissioned by The Swedish Trade Association for Online Gambling.

DownloadGambling Industry Statistics report on the size and shape of the gambling industry in Great Britain.

This brief report provides an overview of Gross Gambling Yield (GGY) by sector, along with the numbers of licensed operators and premises. It is based on data reported to us by the operators we licence and regulate.

This is a revision of the data published in November 2021, in which the inclusion of figures for the most recent period, April 2020 to March 2021, was affected by the impact of restrictions during the pandemic of Covid-19. The lack of and quality of data submissions from some operators and resource required for the consequential quality assurance resulted in a reduced publication which only covered Remote Casino, Betting and Bingo (RCBB), the National Lottery, and the numbers of operators and licences held for this period.

This revision includes data from all the land based non-remote sectors and the society lottery sector which were omitted from the last publication.

The accompanying data file includes figures for all sectors, based on data from April 2020 to March 2021, as well as historical data back to 2009.

This report is useful for anyone who has a business interest in the gambling industry including international regulators, journalists, academic researchers, financial institutions, statisticians and local authorities.

Legitimate interests

There are a number of operations the Code suggests can be based on legitimate interests of the operator subject to a legitimate interest assessment. They include:

- system testing and security measures

- detection of player account fraud

- analytics of trends and forecasting within the player database (assuming this is non-cookie based)

- call recordings for quality assurance and potential dispute resolution

- customer segmentation for promotions and direct marketing purposes – for example, knowing which customers are sportsbook as opposed to casino

- establishment of VIP status based on game history for the purpose of offering special benefits to customers

- chatbot to direct customer queries or requests to the relevant person.

Bosnia and Herzegovina

Despite a relatively small population and a 22.5% decline in betting revenues due to Covid-19, the Bosnia-Herzegovina gambling industry’s turnover amounted to an impressive €700 million in 2020.

As is the case for other federations, Bosnia and Herzegovina lacks gambling laws that apply throughout its territory. Only anti-money laundering and data protection laws are enforced at a federal level.

Each of the three entities that make up the country regulates gambling within its jurisdiction. In the Brčko District, online gambling is banned following the 2004 Law on Games of Chance and Entertainment Games. On the other hand, local licensing is available in both Republika Srpska and the Federation of Bosnia and Herzegovina, thanks to laws published respectively in 2019 and 2015.

Analytical articles

14 September, 2022

Western Europe: big bet, big payoff

In both entities, lotteries are subject to state monopoly. Republika Srpska allows both casino and online betting services to be offered by authorised online operators; the Federation of Bosnia and Herzegovina only allows online betting (excluding virtual sports, which are explicitly banned), and licenses must be tied to a land-based operation.

Romania

By far the most populated country in the region, Romania is home to 19 million people. In 2019, the online gambling industry of Romania raked in €70.2 million. If this seems like a low amount, consider that it represents a 416% increase from 2015, in the face of a meagre 5.5% increase in iGaming’s overall market share during the same period (from 9.5% to 15%). Data from 2020 and 2021 will tell the story of whether the pandemic truly kickstarted the online gaming segment in Romania, but the potential is truly enormous.

Gambling is regulated by the 2009 Gambling Act and the 2016 Gambling Regulation; secondary texts on anti-money laundering measures, technical requirements, advertising, and player protection are currently being discussed.

As far as online services go, the National Gambling Office offers operators separate licenses for casinos, sportsbooks, raffles, and bingo-type games. The lottery is a state monopoly operated by Loteria Romana.

The number of licenses available is uncapped; the cost to start the process is €2,500. Yearly, operators have to pay €13,500 in administrative fees and an amount ranging from €6,000 and €120,000, depending on their turnover. Operators are also required to present a €100,000 guarantee. Taxes amount to 16% of the GGR or €100,000 per year, whichever is higher, plus a monthly levy of 2% of the turnover.

Acknowledgements

MacRae Lynch helped edit the draft manuscript.

4. Catena Media

- Revenue: €106.0 million

- Stock ticker: CTM (NASDAQ)

- Headquarters: Quantum Place, Triq ix-Xatt, Ta’ Xbiex, Gzira

- Number of employees: 404

- Founded: 2012

Catena Media is one of the most successful and respected marketing and affiliate companies in the online gambling space. While the business posts revenues of around €100 million yearly, and €106.0 million for 2020, it remains at the forefront of promoting gambling products in a safe, responsible, and value-added way.

How many online gamblers are there?

The online gambling statistics indicate that 17% of the world’s population enjoys online gambling. The overall percentage of gamblers worldwide is 26%, and this includes all forms of gambling.

(Casino.org)

Mobile Operator of the Year

Alea

SEGMENTATION

Funding

The author and his research group have an overall research support from the state-owned Swedish gambling operator AB Svenska Spel, as well as project-specific funding from the research councils of AB Svenska Spel, and research councils of the Swedish state-owned alcohol monopoly Systembolaget and the Swedish Enforcement Authority. The present study was also funded thanks to an overall research support from the southern Swedish hospital organization (Södra sjukvårdsregionen and Region Skåne).

Methods

Quick overview

- In March 2022, at least 43% of Brits gambled at least once.

- Over a quarter of Brits (27%) have taken part in the National Lottery in 2022.

- As of March 2022 £1,911.8 million was raised for National Lottery projects.

- On average, Brits spend £2.60 per week on gambling, totalling over £135.20 per year.

- The total gross gambling yield stood at £14.1 billion in 2020, which is 1.4% less than the total in 2019

- Gambling addiction is estimated to cost the UK up to £1.27 billion per year.

- The National Lottery contributed £1.6 billion to good causes in 2018/2019.

- £838 million is held in online betting accounts in the UK (April- September 2020)

Online Gambling Market Value Chain Analysis

Our report provides extensive information on the value chain analysis for the online gambling market, which vendors can leverage to gain a competitive advantage during the forecast period. The end-to-end understanding of the value chain is essential in profit margin optimization and evaluation of business strategies. The data available in our value chain analysis segment can help vendors drive costs and enhance customer services during the forecast period.

CONCLUSION

These results suggest that the impacts of COVID-19 on gambling and problematic gambling are diverse – possibly causing a reduction in current or future problems in some, but also promoting increased problematic gambling in others. The longer-term implications of both the reduction in overall gambling, and the increase in some vulnerable groups are unclear, and will be better assessed in subsequent follow-up studies. The surveys reviewed in this paper were conducted at a time when land-based gambling was uniformly unavailable across jurisdictions. The gambling landscape during any follow-up studies will be more variable in terms of restriction (land-based casino openings, online betting caps) that will make examination of overall trends more complex. However, in the short term, individuals with existing gambling problems and other comorbidities need to be recognized as a vulnerable group.

Background

Emerging research has highlighted that the coronavirus disease (COVID-19) pandemic may cause or worsen mental health problems (1) and that this may include addictive behaviors and addiction-like online behaviors (2, 3). Among the latter, problem gambling has been mentioned as a potential consequence of the pandemic and the restrictions surrounding it (4, 5).

Mechanisms potentially increasing gambling behavior during COVID-19 may include effects from the financial crisis and unemployment caused by the pandemic, but also, home confinement and changes in employment and everyday habits may enhance people's time at home and increase the time spent online. Likewise, the nearly total lockdown in sports events in most parts of the world during the early phases of the pandemic changed the gambling market significantly, logically leading to decreased gambling on sports events otherwise popular in gamblers (4). In March 2020, several countries took action in order to prevent a transfer to potentially more addictive types of gambling. Policy makers have expressed fear of gamblers switching to other gambling types, and that such a transfer in gambling habits may push gamblers or subpopulations of gamblers toward more rapid, online-based gambling types (6).

A self-report survey study in Sweden demonstrated that only a relatively limited minority of the population reported an increased gambling behavior during the early phases of the pandemic, but also that this subgroup had markedly higher rates of problem gambling than those reporting decreased or unaffected gambling (7). Likewise, another recent survey study from the same setting displayed findings in line with this; past-month gambling during the spring of 2020 was markedly lower for some gambling types compared to a previous report from the same setting, whereas some other gambling types appeared to be more preserved despite the pandemic. Typically, the more land-based gambling types were more affected by COVID-19-related lockdown and restrictions, whereas online gambling types appeared to be less affected (8). While such findings rely on self-reported data from survey respondents, objective data on gambling activities are needed, in order to demonstrate possible changes and transfers of gambling habits within the gambling market and between different types and modalities of gambling. One study on measured gambling data from one (anonymous) gambling operator demonstrated a modest impact from COVID-19 on gambling behavior, such that migration from sports betting to online casino within that specific operator could not be demonstrated (9). In contrast, however, a different study conducted in Ontario, Canada, demonstrated that some migration was likely between gambling types, due to the pandemic (10). Thus, findings are hitherto diverse with respect to the pandemic's consequences on gambling behavior, and further data are needed, if possible from objective sources of non-self-report gambling data.

Thus, the present study used official, national authority data on revenue-based taxation from gambling operators, aiming to study measures of financial activity in the overall legal gambling market in Sweden and the activity of specific subsections of the market. In the study, it was hypothesized that activity in the gambling market would have decreased in the gambling types related to sports events and other land-based gambling and that an increase may be possible in online-based gambling involving other types of gambling. Also, the study aimed to study whether decreases in some gambling types may be fully or partly counteracted by increases in other gambling types.

New articles

An Assortment of the Best Slots of 2021 Casumo Blog

Mechanics, themes, and bonus features of the best slots released each month of 2021 featuring some of Casumo’s favourite new slots.

Download Royal Vegas Android App To Play Slots In Ireland

How to download Royal Vegas Android app to play slots In Ireland? Download the online casino app for Android or iPhone and play slots, table games.

Friends Slots - Free Play Online Slot Machine Game

Play xxxxxx slots for free or real money. Genuine Las Vegas slots, play for free with no download, and no spam

Wild tornado value pack, caesar casino login – Profile – Ski/Snowboard/Kiteboard/wakeboard DIY builder Forum

Ski/Snowboard/Kiteboard/wakeboard DIY builder Forum - Member Profile > Profile Page. User: Wild tornado value pack, caesar casino login, Title: New Member, About: Wild tornado value pack ...

Big money made on social apps as gambling and gaming collide

Regulations prohibiting gambling on social media in Australia are being increasingly challenged by the popularity of casino apps for iPhones and Androids, as well as loopholes exploited by offerings on…

Online Slots| Genesis Casino

There’s a plethora of Online Slots available at Genesis Casino. You can choose from a wide range of themes from classic fruit games to adventurous games.